KEY TAKEAWAYS

- The LPL Research Corporate Beige Book Barometer continues to exhibit upbeat sentiment from companies during the third quarter of 2017.

- About 60% of S&P 500 companies mentioned hurricanes during their conference calls, highlighting the broad impact.

- The positive tone from management teams appears to support a positive near-term earnings outlook even without factoring the potential benefits from tax reform.

CORPORATE BEIGE BOOK: UPBEAT AS EXPECTED

Companies remained generally upbeat during the third quarter earnings season, based on the LPL Research Corporate Beige Book Barometer. This is hardly surprising, given actual earnings results were good again and estimates of future earnings held up relatively well as companies provided forward-looking guidance.

Earnings call transcripts analyzed took place starting in mid-October extending through the third week of November.

POSITIVE SENTIMENT CONFIRMS EARNINGS STRENGTH

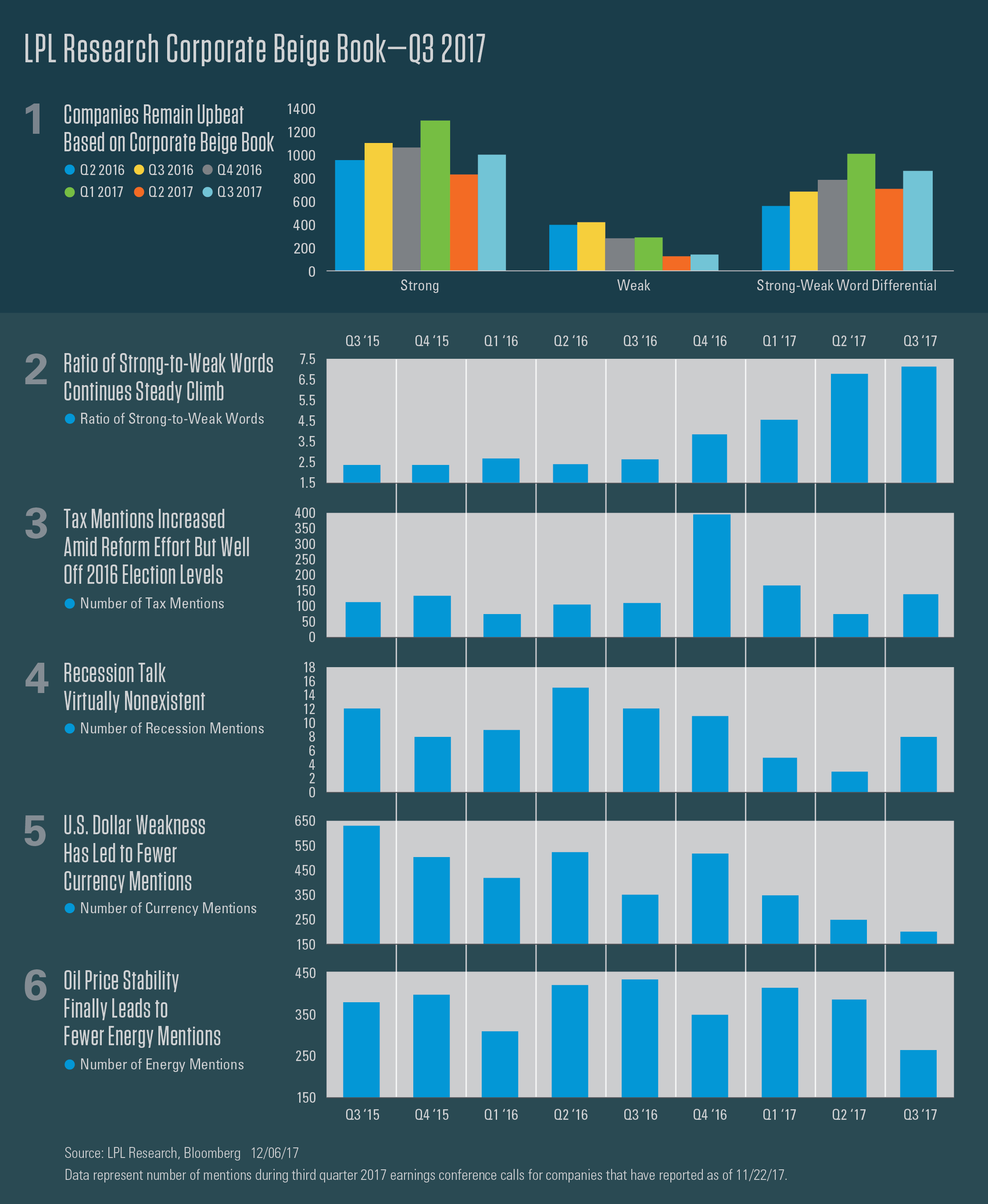

Corporate sentiment remained very upbeat during the third quarter based on our count of positive and negative words in earnings conference call transcripts. We observed a pickup in strong words, little change in the number of weak words, and a resulting increase in the differential between strong and weak words, which remains very positive [Figure 1]. Accordingly, the ratio of positive-to-negative words continued its steady climb since the end of the China and oil-driven downturn in spring of 2016 [Figure 2]. Specifically, from the third quarter of 2016 to the third quarter of 2017, the ratio of strong-to-weak words rose steadily from 2.6 to 7.1.

The improvement in management sentiment is encouraging and consistent with the strong earnings season and generally upbeat guidance. We believe the positive tone from management teams supports our outlook for the potential of more solid earnings gains next year, as noted in our Outlook 2018: Return of the Business Cycle.

Here are some excerpts from call transcripts supporting the positive sentiment on the macro environment:

- “With respect to customers, the feedback from discussion with customers is I think pretty optimistic about their prospects, what they’re seeing in terms of demand.” - Vehicle Manufacturer

- “As we move into the fourth quarter, the macroeconomic environment looks solid. We also remain confident about the holiday season, as consumer sentiment remains elevated. Looking outside the U.S., global growth projections have moved higher as performance in Europe and China continues to exceed expectations.” - Transport

- “The economy from our perspective continues to look steady. Customers continue to be somewhat optimistic, there’s a bit more optimism about fiscal or tax reform and the ability to see that improved growth rates in the economy.” - Bank

POLICY FOCUS CENTERED ON TAX REFORM

While the amount of attention corporate management teams have paid to the Trump administration on their earnings calls has fallen in recent quarters, tax reform has continued to get a lot of air time [Figure 3]. The tax issue got more attention during the November 2016 election, but mentions in transcripts we analyzed roughly doubled from the second quarter to the third as the bills worked their way through Congress. Specifically, the word “tax” or its variants were mentioned over 400 times during fourth quarter 2016 earnings conference calls before falling to below 70 in the second quarter of 2017 and then rising to 126 last quarter. Mentions of other key policy initiatives were little changed and fairly infrequent, although “infrastructure” got a bump from 18 in the second quarter to 33 in the third.

Here are some executives’ comments on Washington, D.C. policy initiatives:

- “I think there will be a good uptick in terms of investment … so I’m pretty optimistic that the new tax law will be a good catalyst for growth.” - Engineering and Construction

- “While the economic outlook remains fairly promising, we see further upside potential from U.S. tax reform, which we strongly support. The current proposal will provide great incentives for companies to both reinvest and create jobs at home.” - Transport

- “It is important that Washington and the business community unite now behind a tax reform bill that will have a positive impact on domestic jobs and on economic growth. Still remaining optimistic that something on this front can get done, we are not assuming reform in our 2017 guidance.” - Healthcare

- “Our commercial clients remain optimistic. They continue to look forward to continued implementation of a pro-growth agenda, particularly focused on meaningful tax reform.” - Bank

- “We support a pro-growth tax reform package, a significantly lower marginal rate, and we’re prepared to see certain preferences changed or eliminated. We think that will drive economic growth, which is a key factor in terms of our growth as a company.” - Insurer

STILL VERY LITTLE TALK OF RECESSION

Corporate executives generally try to stay away from the “R” word (recession) when talking with investors, confirmed by the small number of mentions of the word over the past several years. The word “recession” got a tiny bit more use in the third quarter [Figure 4], but its use is either international, e.g., Europe has escaped recession or Brazil is climbing out, or it is simply a reflection back to the Great Recession. Bottom line, recession is hardly a part of corporate managements’ vocabularies at this point, which along with our assessment of leading economic indicators, points to a very low probability of recession in the near term.

WEAKER DOLLAR LED TO FEWER MENTIONS

The amount of attention on currencies has fallen dramatically over the past two years, reflecting the stability and then weakness in the U.S. dollar. Recall a strong dollar is a drag on overseas earnings by U.S.-based multinationals, while a weak dollar provides a currency translation benefit.

Currency mentions fell 19% from the second quarter to the third, after roughly 30% drops during the prior two quarters [Figure 5]. That trend follows the path of annual changes in the dollar, which have gone from +3.6% (Q1 2017) to +4.1% (Q2 2017) to -2.4% (Q3 2017) and are estimated to be -6% in the fourth quarter of 2017 (based on the U.S. Dollar Index). Currency had a slight but barely discernable impact on overall S&P 500 earnings in the third quarter, and was therefore not needed as an excuse for shortfalls relative to expectations. During the fourth quarter, it is possible that a larger currency benefit gets more attention.

Here are several management comments on currency reflecting the tailwind:

- “The currency translation effects went from being a headwind to actually being a slight tailwind.” - Capital Goods

- “Our sales growth of more than 3% was driven by improving sales volume and favorable currency translation.” - Materials

- “In terms of currency translation, we received a tailwind of a half percent to one percent. We’re benefiting from dollar weakness most significantly versus the euro.” - Payment Processor

Our U.S. dollar view is slightly positive in 2018 due primarily to the divergences in global monetary policy, as discussed in Outlook 2018.

ENERGY GETTING LESS ATTENTION

The number of mentions of “oil” (and related “fuel”, “gas”, or “crude”) dipped during the third quarter [Figure 6] – not surprising given recent oil price stability relative to the extreme volatility in late 2015 and early 2016. What is surprising however, is that the number of mentions remained elevated during the second half of 2016 and first half of 2017, despite energy’s strong rally off of the early 2016 lows. Many of those mentions were in a positive context, as higher oil prices helped, and energy companies will always comment on energy prices, but we are still surprised that it took this long for energy to fall off of companies’ radar in a meaningful way.

CONCLUSION

Management sentiment during third-quarter earnings season was again quite positive, which is not surprising given that actual earnings results were solid and forward estimates held up very well. The hurricane drags were evident in the numbers and comments from management teams. Still, we believe the overall positive tone from corporate America during earnings season supports a positive outlook for earnings growth through year-end and into 2018.

We are saddened by the passing of Rich Yamarone, Bloomberg Economist, whose work was critical to our Corporate Beige Book analysis.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

Because of its narrow focus, specialty sector investing, such as healthcare, financials, or energy, will be subject to greater volatility than investing more broadly across many sectors and companies.

The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings.

Currency risk is a form of risk that arises from the change in the price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

All investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Russell 1000® Growth Index measures the performance of those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values. Russell 1000® Value Index measures the performance of those Russell 1000 companies considered undervalued relative to comparable companies.

This research material has been prepared by LPL Financial LLC.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial LLC is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

Tracking #1-676273 (Exp. 12/18)