Balanced Risk Reward

John Lynch Chief Investment Strategist, LPL Financial

Jeffrey Buchbinder, CFA Equity Strategist, LPL Financial

Key Takeaways

- We are readjusting our recommended domestic equity allocations back to market weight.

- Following the stock market’s recent move higher, coupled with a slightly weaker economic and corporate profit outlook, the risk-reward trade-off in stocks has become less attractive.

- From a technical perspective, consolidation of recent gains in the S&P 500 Index may be necessary, though we do not expect a retest of the December 2018 lows.

Macro Outlook Less Certain

This change in asset allocation is driven by more recent stock market strength than deteriorating fundamentals. However, we acknowledge that the U.S. economy has hit a soft patch to the start the year and other elements of the macroeconomic backdrop have weakened:

- Economic soft patch. Since the start of the year, consensus forecasts for first-quarter gross domestic product (GDP) growth have fallen to 1.5% from 2.3%, based on Bloomberg consensus forecasts. Ongoing trade uncertainty, slower growth overseas—particularly in Europe—and the record-long government shutdown are among the reasons for the sluggish growth. The good news is that this is consistent with previous first-quarter readings this cycle, and some temporary headwinds are expected to clear, setting up a pickup in growth in the second quarter. In addition, the consumer spending outlook remains solid, buoyed by continued gains in employment and wages.

- Stalling capital investment. Disappointing capital investment in recent quarters is partly due to ongoing trade uncertainty and weaker business confidence. The weaker business investment environment is evidenced by the dip in manufacturing surveys from the Institute for Supply Management since last fall. Moreover, in large part due to trade uncertainty, the fiscal stimulus put in place as part of tax reform in 2017 has not driven quite as much capital spending as we anticipated. We still expect an eventual U.S.-China trade deal to help shore up business confidence and lead to more investment as U.S. businesses take advantage of improved incentives for investment, including immediate expensing.

- Slower earnings growth. Though S&P 500 earnings estimates tend to come down over the course of a calendar year, the recent drop is greater than the historical average. Consensus now expects a 4% increase in S&P 500 earnings in 2019, with the possibility of a slight decline in the first quarter, according to FactSet. At this point, we’re maintaining our 2019 earnings per share (EPS) estimate of $172.50 for the S&P 500 Index, representing about 6% growth. When we initiated this forecast, our number was 3 percentage points below Wall Street consensus. Over the past several months, consensus estimates have fallen to 2.5 percentage points below our estimate, which we believe may be overly pessimistic. Solid economic growth and clarity on trade may result in earnings closer to our number.

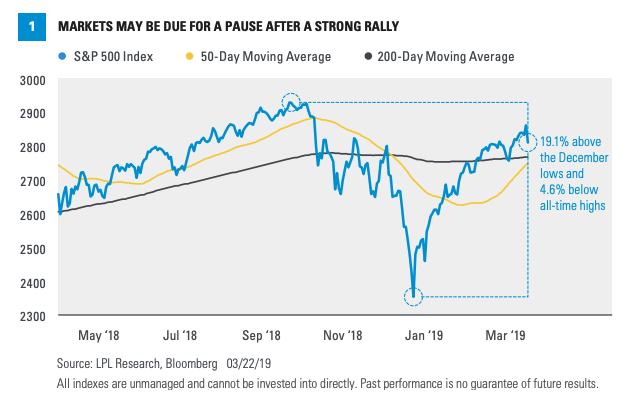

Technical Perspective

We believe a more cautious stance on equities may also be warranted based on technical analysis. Given the significant run-up in prices over the past few months, along with likely weakness in first quarter GDP and corporate profits,

The bond market is also sending cautious signals with the sharp move lower in yields, the latest leg down coming after last week’s Federal Reserve meeting, which indicated the likelihood of no more interest rate hikes in 2019. The latest drop in the 10-year yield brings the U.S. Treasury yield curve teetering on the edge of inversion (when long-term yields fall below short-term yields). That worrisome signal has preceded each of the past nine recessions going back to 1955.

We would note that even after the yield curve inverts, recession doesn’t historically follow for quite some time, and during that time stocks have fared quite well. Specifically, looking at the past five recessions, the economy continued to expand for an average of 21 months after the yield curve inverted, and the average gain in the S&P 500 to its eventual peak was over 20%. We aren’t ignoring this potentially troublesome signal from the bond market, but it doesn’t appear to be the major warning that some think it is.

Bottom line, some near-term consolidation is reasonable to expect; however, we continue to think fundamentals are favorable.

Potential Risks for Investors to Consider

- Although we expect corporate profits and a steady economy to support stocks in 2019, there are a few potential scenarios to watch for:

- Increased costs could weigh on companies’ profit margins and hurt profits.

- U.S.-China trade negotiations could be prolonged and pressure market sentiment.

- The global economy may slow more than expected.

- Signals of weaker growth from the bond market may prove to be correct.

- Structural challenges in Europe (Brexit and Italian debt) and Japan (upcoming consumption tax) may be bigger drags on growth than the market expects.

Downside risk increases with stocks at higher levels, despite what we still think is a generally favorable macroeconomic backdrop. This shifting risk-reward balance leads us to our market weight stance for domestic equities within our recommended asset allocation. The goal is to better position diversified portfolios for potential stock market consolidation, while enabling them to participate in future market gains with a more balanced portfolio structure as the business cycle ages further.

Conclusion

We still think stocks will be higher at year end than they are now, despite potentially slower economic and earnings growth alongside other risks noted above. We expect steady,

Thank you to Ryan Detrick and Scott Brown for their contributions to this report.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in this material may not develop as predicted.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee

All indexes are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure

DEFINITIONS

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share

This research material has been prepared by LPL Financial LLC.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial LLC is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

RES 95140 0319 | For Public Use | Tracking #1-835483 (Exp. 03/20)