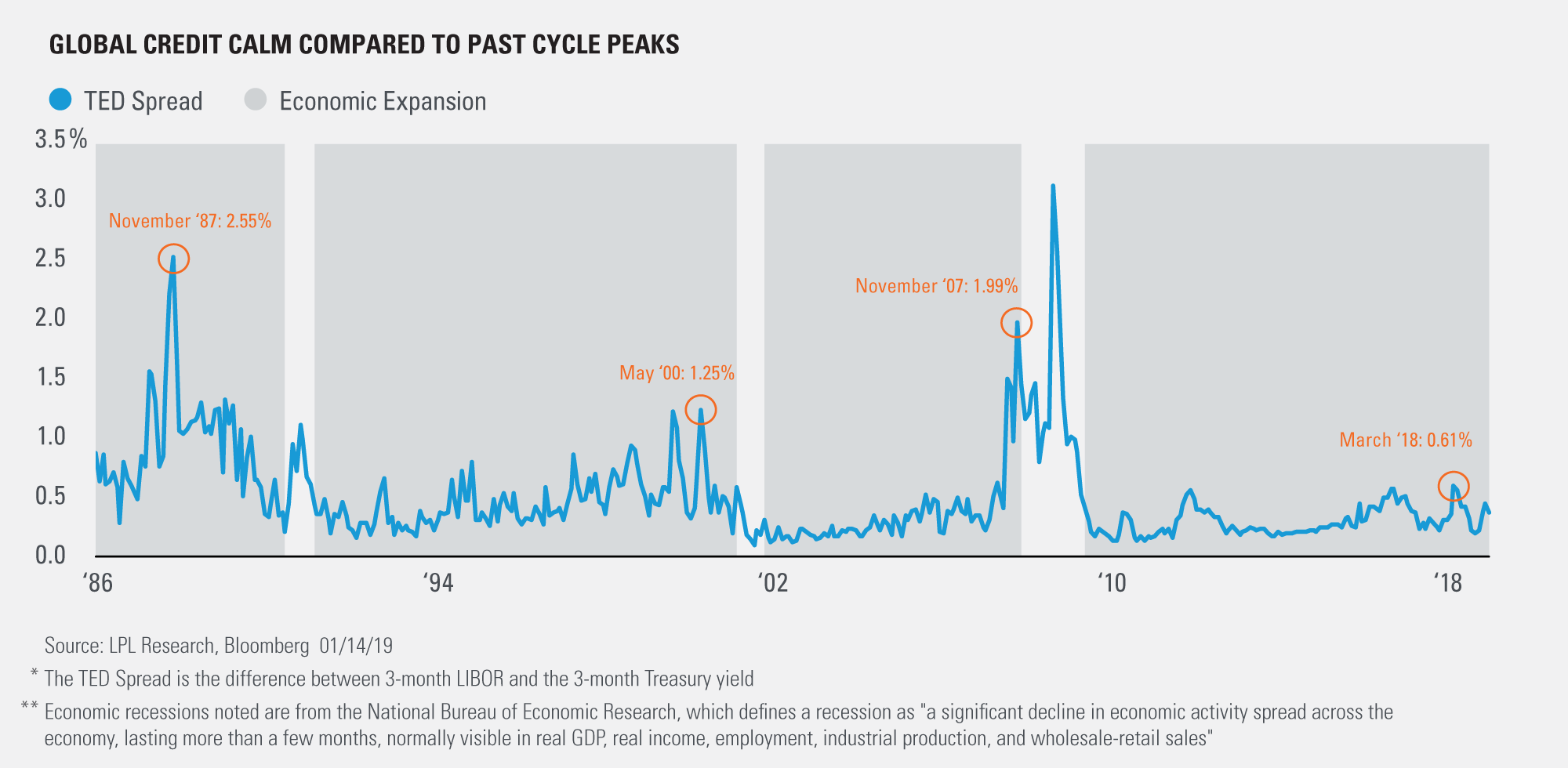

Credit stress among banks has remained relatively calm recently, signaling an economic recession may not be as imminent as some investors fear.

As shown in the LPL Chart of the Day, the TED spread, or the difference between the 3-month London Interbank Offered Rate (Libor) and the 3-month Treasury yield, climbed above 1% in the 12 months before each of the last three recessions, a level that hasn’t been breached in the current cycle.

The TED spread has climbed as high as 0.61% during this cycle, a level it reached in March

To us, the relative quiet in banking credit is a testament to moderating, but solid global demand supported by strong U.S. economic trends. Investors have endured several headwinds recently, including a prolonged U.S.-China trade dispute, geopolitical issues, and signs of slowing international demand. Still, we feel encouraged by

“Even though the global environment has become more tenuous, companies’ balance sheets remain strong,” said LPL Research Chief Investment Strategist John Lynch. “We do not anticipate a recession in 2019, thanks to solid economic momentum and significant fiscal tailwinds.”

As mentioned in our Outlook 2019: FUNDAMENTAL: How to Focus on What Really Matters in the Markets, we forecast global gross domestic products (GDP) growth of 2.5-2.75% in 2019. Although we are late in the cycle, this period can last a long time, and we have yet to see the excesses of “red flags” (like a blowout in the TED spread) that have historically signaled economic peaks.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual security. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. The economic forecasts set forth in this material may not develop as predicted.

All indexes are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. All performance referenced is historical and is no guarantee of future results.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments.

This research material has been prepared by LPL Financial LLC.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial LLC is not an affiliate of and makes no representation with respect to such entity.

The investment products sold through LPL Financial are not insured deposits and are not FDIC/NCUA insured. These products are not Bank/Credit Union obligations and are not endorsed, recommended or guaranteed by any Bank/Credit Union or any government agency. The value of the investment may fluctuate, the return on the investment is not guaranteed, and loss of principal is possible.

Member FINRA/SIPC

For Public Use | Tracking # 1-811906 (Exp. 01/20)