An Aging Cycle

John Lynch Chief Investment Strategist, LPL Financial

Barry Gilbert,

Callie Cox Senior Analyst, LPL Financial

Key Takeaways

- The current economic expansion will become the longest ever in July.

- Slow (but steady) growth and accommodative policy have made this expansion especially durable.

- We still see many signals that this cycle could persevere at least through the end of 2019.

The tenth anniversary of the S&P 500 Index bull market is coming up on March 9. As the U.S. stock rally’s double-digit birthday nears, we’ve reflected a lot on the durability of the current economic cycle. The U.S. economic expansion is entering its 118th month, on track to become the longest recovery on record in July.

Some things in life get better with age, but recession calls have grown louder recently amid heightened global uncertainty and market volatility. While it is important to be mindful of where we are in the cycle, we see a lot of evidence that this economic cycle has enough fuel left in the tank to persevere at least through the end of this year and could prove durable.

Slow, but Steady

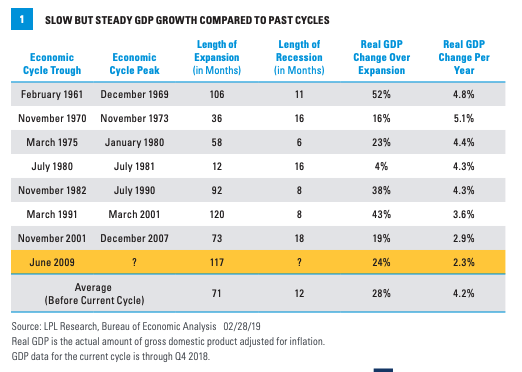

In past economic cycles, slow but steady growth has won the race. Since 1970, cycles with annual gross domestic product (GDP) growth higher than 4% lasted about five years on average, while cycles with annual growth lower than 4% lasted about nine years on average [Figure 1]. While slow growth in this cycle has been frustrating at times, especially after a swift and painful downturn, it has helped extend the life of this cycle and keep excesses in check. Inflation-adjusted GDP has expanded an average of 2.3% annually in this cycle, the slowest pace of growth among all expansions in recent memory, and a key contributor to the expansion’s near-record age.

Steady economic growth has been helped in part by extraordinary supportive monetary policy for much of the cycle and a cautious, gradual approach to tightening. The Federal Reserve’s (Fed) supportive policy efforts have been in place for many years, but policymakers only started increasing rates in December 2015, more than six years into the expansion. Since then, the Fed has implemented nine 25-basis point (.25%) hikes, matching the slowest Fed hiking pace in tightening cycles since 1970. This tightening cycle is one of the longest on record, yet inflation-adjusted interest rates are barely above zero. Inflation (measured by core personal consumption expenditures) has been climbing since 2015, but it’s only hovering around the Fed’s 2% target, and wage growth, while healthy, remains manageable. Muted inflation can be attributed to several structural factors like demographics and globalization, but the Fed has played a pivotal role in promoting stable pricing while restricting growth only minimally. We believe this pragmatic and gradual approach will continue to be effective, and we see minimal chances of a policy mistake en route to a soft landing from the current modest slowdown.

The lingering effects of fiscal stimulus may also provide an extra boost to the expansion, especially if companies ramp up capital expenditures once we see a United States-China trade resolution. Supply-side fiscal stimulus can have a positive impact on output for several years as consumers and businesses reap the benefits of tax cuts and fiscal incentives.

Encouraging Data

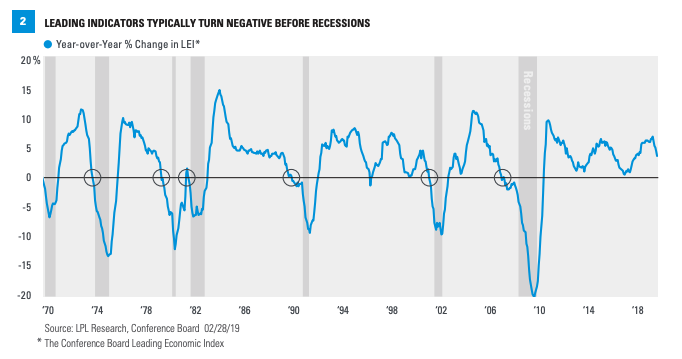

While we’ve noted recently that coincident economic reports have sent mixed messages about economic conditions, leading economic data

Other indicators we track in our Recession Watch Dashboard also show low odds of a recession over the next 12 months.

Global Liquidity

We’ve highlighted how the Fed’s accommodation has supported economic growth over the past several years. However, the United States’ current economic expansion has also benefitted from a wave of central bank accommodation across the globe, thanks to a staggered global economic recovery. Balance sheets for major central banks are still around the biggest they’ve been since the financial crisis amid tepid growth internationally, and interest rates are low worldwide, incentivizing borrowing and investment. This accommodative environment (and resulting global growth potential) will likely continue to support the domestic recovery, especially as the Fed pauses on rate hikes. The Fed has also communicated that it will be flexible on reducing the size of its own balance sheet and will likely maintain a larger balance sheet compared to before the 2008 financial crisis.

Ample accommodation this late in a cycle can potentially contribute to a build-up in economic excesses. However, we have yet to see any alarming signs of late-cycle excesses of “red flags” in the economy.

Conclusion

While it’s important to be mindful of where we are in the economic cycle, later-cycle economies can continue to exhibit stable growth for years. We’re maintaining our positive outlook for 2019, thanks to our conviction in sound fundamentals supporting moderate economic growth. At the same time, we remain on watch for any threatening signs of slowing or excess, and we’ll continue to keep an eye on trusted economic and market signals.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in this material may not develop as predicted.

Investing involves risk including loss of principal. No investment strategy or risk management technique can guarantee

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

This research material has been prepared by LPL Financial LLC.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial LLC is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

RES 86204 0219 | For Public Use | Tracking #1-828237 (Exp. 03/20)