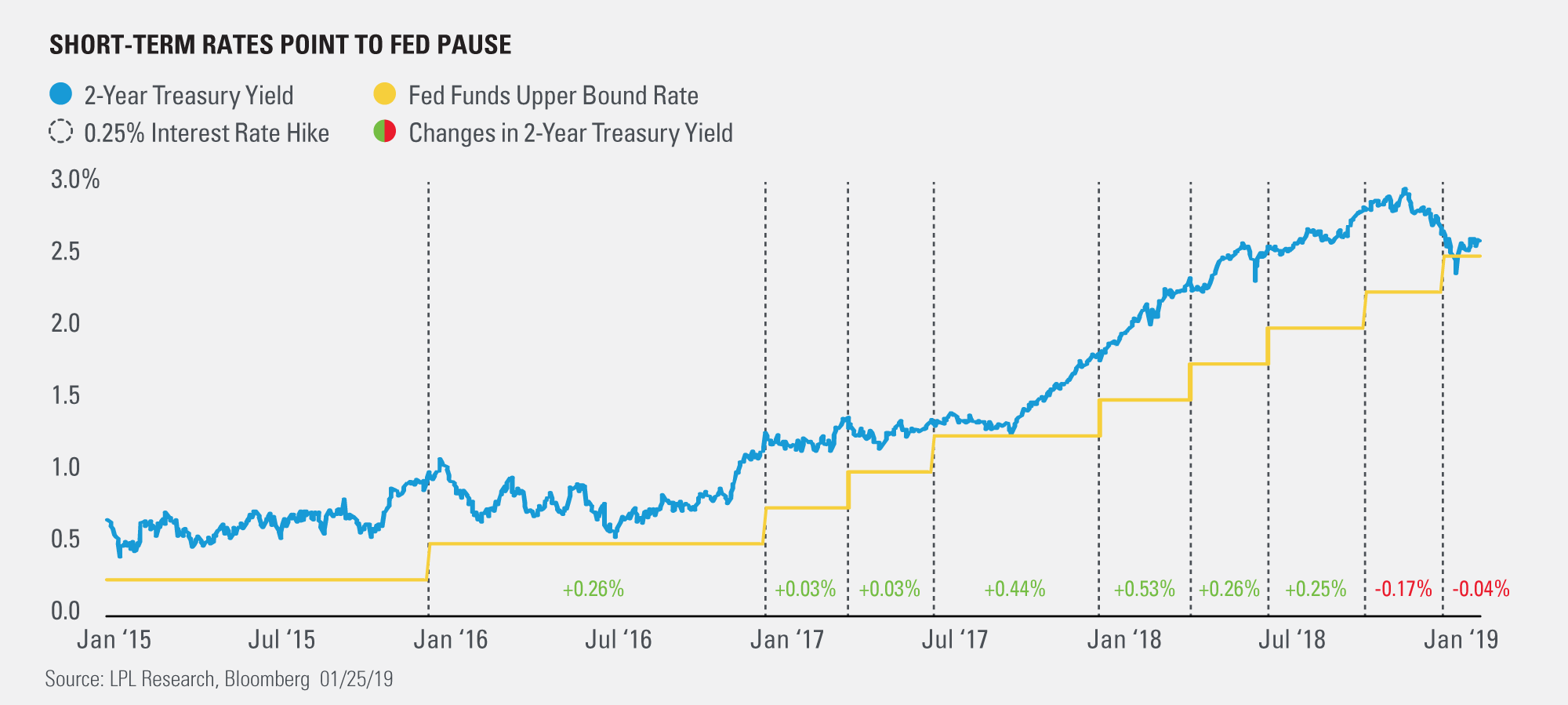

Investors have increasingly positioned for a Federal Reserve (Fed) pause, which could portend a shift in fixed income markets. Fed fund futures are pricing in about a 70% probability that the Fed will keep rates unchanged for the rest of 2019, and the market’s dovish tilt has weighed on short-term rates.

As shown in the LPL Chart of the Day, the 2-year yield has typically followed the fed funds rate since policymakers began raising rates in December 2015. While we expect one or two more hikes this cycle, there is a possibility that the Fed’s December hike was its last, which will likely cap short-term rates.

Short-term yields have outpaced longer-term yields over the past few years, flattening the yield curve and raising concerns that U.S. economic progress may not be able to keep up with the Fed’s tightening. The spread between the 2-year and 10-year yield has fallen negative before every single U.S. recession since 1970.

If the Fed pauses, the curve will likely reverse course and steepen as solid economic growth and quickening (but manageable) inflation drives longer-term yields higher. As mentioned in our Outlook 2019, FUNDAMENTAL: How to Focus on What Really Matters in the Markets, we’re forecasting the 10-year Treasury yield will increase significantly from current levels and trade within a range of 3.25-3.75% in 2019.

“We remain optimistic about U.S. economic growth prospects, and recent data show inflation remains at manageable levels,” said LPL Research Chief Investment Strategist John Lynch. “Because of this, we expect the data-dependent Fed to be less aggressive than initially feared, as policymakers juggle these factors with the impacts of trade tensions and tepid global growth.”

To be clear, investors shouldn’t fear a flattening yield curve given the backdrop of solid economic growth and modest inflation. Historically, the yield curve has remained relatively flat or inverted for years before some recession started. Since 1970, the United States has entered a recession an average of 21 months after the yield curve inverted.

We’ll be monitoring the Fed’s rate announcement and post-meeting comments for any signals on future policy moves. For more of our thoughts on the Fed’s upcoming meeting and financial markets’ reactions, check out our latest Weekly Economic Commentary and Weekly Market Commentary.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual security. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. The economic forecasts set forth in this material may not develop as predicted.

All indexes are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. All performance referenced is historical and is no guarantee of future results.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments.

This research material has been prepared by LPL Financial LLC.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial LLC is not an affiliate of and makes no representation with respect to such entity.

The investment products sold through LPL Financial are not insured deposits and are not FDIC/NCUA insured. These products are not Bank/Credit Union obligations and are not endorsed, recommended or guaranteed by any Bank/Credit Union or any government agency. The value of the investment may fluctuate, the return on the investment is not guaranteed, and loss of principal is possible.

Member FINRA/SIPC

For Public Use | Tracking # 1-816502 (Exp. 01/20)