CORPORATE AMERICA IMPRESSES AGAIN

John Lynch Chief Investment Strategist, LPL Financial

Jeffrey Buchbinder CFA Equity Strategist, LPL Financial

KEY TAKEAWAYS

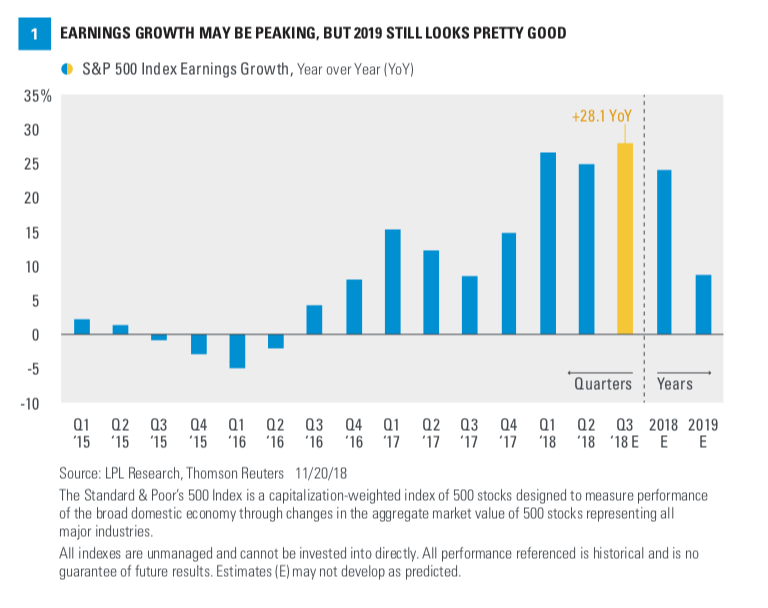

- Third quarter earnings season was again very impressive, with S&P 500 Index earnings growing 28% year over year, the fastest pace since the fourth quarter of 2010.

- A pickup in economic growth, strong manufacturing activity, and tax cuts were the key growth drivers.

- Guidance was generally positive despite tariffs and ongoing trade policy uncertainty.

Corporate America produced another outstanding earnings season. We expected another quarter of strong earnings growth, and corporate America delivered even more than we anticipated. Third quarter numbers were excellent, even if the boost from the new tax law is excluded, as has been the case throughout this year. Revenue and earnings upside compared with expectations was particularly impressive, making prior assertions of an earnings growth peak premature. We’re also impressed by the resilience of companies’ outlooks in the face of tariffs and ongoing trade policy uncertainty.

BY THE NUMBERS

S&P 500 Index earnings rose 28% year over year [Figure 1], exceeding the second quarter’s 25% pace while outpacing estimates by more than 6%, according to Thomson Reuters’ data. Index earnings have now exceeded consensus estimates for 38 consecutive quarters, based on Thomson Reuters’ data, with double-digit growth

in six of the past seven quarters. A solid 78% of companies exceeded earnings targets, while the revenue beat rate is 61%; both figures are above long-term averages. Even when excluding the impact of the new tax law—conservatively estimated at 7–8 percentage points—earnings growth came in at around 20%.

A pickup in economic growth, strong manufacturing activity, and tax cuts were the biggest drivers of the strong growth, while currency translation from a strong dollar had only a marginal negative impact. At the sector level, technology and financials were the biggest contributors to the overall earnings increase, while rising oil prices helped drive another big increase in energy sector profits.

ELEPHANT IN THE ROOM: TRADE

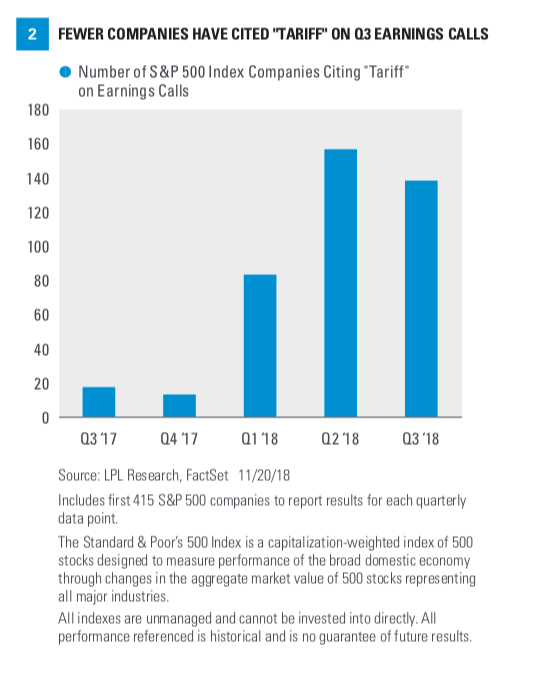

Not surprisingly, trade has been by far the most popular topic on earnings conference calls. The good news is that a significant majority of companies have indicated that the impact from tariffs has been limited thus far. According to a Bank of America Merrill Lynch study, only 9% of S&P 500 companies indicated tariffs had a negative impact during the quarter. Export-focused industrial companies have talked trade the most, followed by consumer discretionary, which makes sense given retailers are heavy importers.

Somewhat surprisingly, trade has received slightly less attention on third-quarter earnings calls than it did in the second quarter [Figure 2]. That may be because tariffs were more of a surprise during the summer months. It’s possible that companies may not be as prepared as we would like them to be, but given the uncertainty, it’s probably prudent for them to take a wait-and-see approach before relocating supply chains.

Sources such as Bloomberg, FactSet,

and Standard & Poor’s have different calculations than Thomson Reuters for S&P 500 earnings, based on various methodologies and different interpretations of what constitutes operating earnings.

MARGIN WATCH

Operating margins for S&P 500 companies remain in an uptrend, in part because of the recovery in

the energy sector from depressed oil prices in 2017. Companies continue to do a good job managing costs and using technology to improve productivity. However, margin headwinds are building. The biggest component of corporate costs is wages, which are rising amid a tight labor market. Also, borrowing costs are increasing as interest rates rise, and tariffs have increased costs for certain manufacturers. Input costs, particularly oil, have been cooperating and tariffs could potentially go away, but we think it’s fair to say that margin expansion opportunities in coming quarters may be limited.

That doesn’t mean earnings won’t grow at a solid pace in 2019, but revenue growth, which is tied to economic growth, may have to do the heavy lifting. We acknowledge the risks that tariffs may potentially be increased and be maintained throughout 2019 (though we see the risk as low), potentially impairing profit margins.

GENERALLY UPBEAT GUIDANCE

Company guidance has mostly been upbeat

during reporting season. During October and November, S&P 500 earnings per share estimates for the next four quarters have fallen by 1.1%, better than the long-term historical average decline of roughly 2%. Considering ongoing trade policy uncertainty, we view this result as positive. There is little if any tax cut boost to estimates here, given tax reform was already in analysts’ estimates, so we think resilient estimates reflect a favorable economic environment.

PEAK IS PROBABLY IN. NOW WHAT?

For the past two quarters, market participants have been focused on whether earnings growth may be peaking (not to be confused with a peak in the absolute level of earnings). Though recent growth rates are unlikely to be repeated in the fourth quarter or in 2019, we still believe the earnings outlook is healthy enough to keep this bull market going through next year and likely beyond. Also, keep in mind that economic recessions historically have not arrived until roughly four years after prior earnings growth peaks.

CONCLUSION

Our lofty expectations for third quarter earnings season have been surpassed. Upside to estimates and growth rates impressed. But markets are forward looking, making guidance paramount. On that score, results were also quite good, with a below-average and modest reduction in forward estimates (Thomson Reuters consensus estimates for 2019 reflect a 9% increase over 2018, following recent estimate cuts). Tariff uncertainty remains

and wage pressures may cap profit margin expansion, but we think the macroeconomic outlook is strong enough to support potential high-single- digit earnings growth for the S&P 500 in 2019.

Those earnings gains, should they be realized (putting S&P 500 earnings per share for 2019 in the $173–174 area), should be sufficient to keep the bull market going through 2019 and likely beyond. Shorter term, potential improvement in prospects for a U.S.-China trade agreement and a more dovish Federal Reserve may support stock market gains over the final five weeks of 2018, even though volatility may be elevated.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

Because of its narrow focus, specialty sector investing, such as healthcare, financials, or energy, will be subject to greater volatility than investing more broadly across many sectors and companies.

All investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

This research material has been prepared by LPL Financial LLC.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial LLC is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit.

RES 43147 1118 | For Public Use | Tracking #1-795994 (Exp. 11/19)