Market Update

- Stocks begin week on cautious tone. U.S. equities are trading flat this morning after strong returns on Friday from the technology and healthcare sectors helped the S&P 500 break a three-week losing streak; though consumer staples, telecom, and utilities all had significant losses last week. Overseas, Asian markets were mixed in Monday’s session as the Nikkei recouped most of a nearly 2% intraday decline, while the Shanghai Composite advanced 0.6%. Meanwhile, disappointing Eurozone Purchasing Managers’ Index (PMI) data have European markets sitting close to session lows. Elsewhere, the dollar will look to build on three weeks of gains amid hawkish Federal Reserve Bank (Fed) comments. WTI crude oil is down over 1.5% and COMEX gold has dipped below its 50-day moving average. Treasuries are mixed, with yields on the 10-year note sliding several basis points.

Macro View

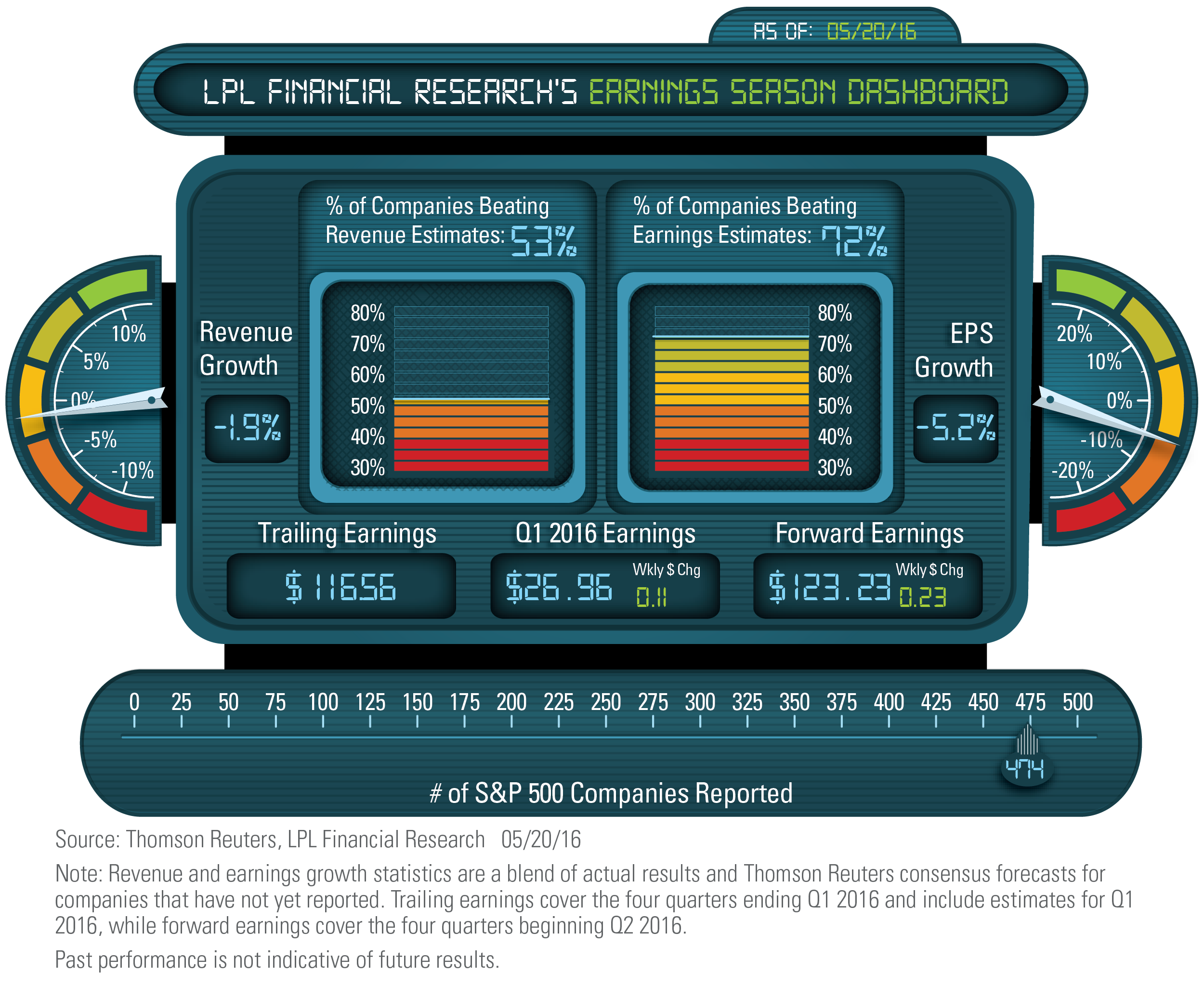

- Estimates inched higher over the past week. S&P 500earnings per share (EPS) for the first quarter of 2016 are down 5.2% year over year, a slight improvement over the past week. More impressive was last week’s increase in estimates over the next four quarters, despite a challenging environment for retailers. Forward estimates for the S&P 500 are down just 1.2% since earnings season began, while the ratio of negative-to-positive preannouncements during reporting season, at 2.2, has been very good relative to historical averages of 2.7 (Thomson Reuters data) and much better than the year ago level (3.8).

- A slight win for the week. The S&P 500 managed a 0.6% gain on Friday to close slightly positive for the week. Technically, the S&P 500 found resistance on Friday right near its 50-day moving average. For the week, financials were the big winner, as potentially higher interest rates helped the rate-sensitive group. On the downside, utilities were the big loser, as this group historically has moved inversely with rates.

- The S&P 500 in a historically tight range. The S&P 500 first closed above the 2,000 level 22 months ago in August 2014, and since then it has traded in a historically tight range. In fact, over the past 22 months the S&P 500 has traded in just a 17.9% range, which is only one of four times the range has been below 20% over a 22-month span. The other times were in 1984, the mid-1990s, and 2005-06. Today on the LPL Research blog we will take a closer look at what this could mean.

- Additional data from Europe show slowing growth.European-wide Purchasing Managers’ Index (PMI) data were released overnight, showing a slowdown from 53 to 52.9, a modest decline when a slight gain was expected. Data released earlier had shown a slight increase from major countries like France and Germany, suggesting that the European economy slowed, if not outright contracted, in the periphery. The European (ex-U.K.) economy grew at 0.5% last quarter. This latest round of data suggests that growth will not be as strong going forward.

- May 21, 2016, was the anniversary of the S&P 500’s all-time high. In this week’s Weekly Market Commentary, due out later today, we take a look at what the stock market’s lackluster performance since the last record high might mean for the current bull market, now the second longest since 1950. One-year periods without new highs have historically preceded strong stock market gains when taking place during bull markets. Still, a comparison of the market environment today compared with a year ago is consistent with our expectation for a volatile, range-bound stock market for the balance of 2016.

- This week’s Weekly Economic Commentary focuses on China and its large debt problem. The numbers on Chinese debt are scary on the surface and are a very real source of concern. However, the situation, while serious, is not without hope. Unlike many other highly indebted countries, China owes most of its debt to itself. This fact, combined with China’s high levels of foreign currency reserves and savings rate, suggests that China’s debt problem is more nuanced than most people realize.

- Week ahead. Fed Chair Janet Yellen and Greg Mankiw, who headed up the Council of Economic Advisors under President Bush, will hold a panel discussion at Harvard on Friday. May 27. Former Fed Chair Bernanke will also join the discussion. On the domestic data front, reports on home sales and durable goods imports and exports for April will draw most of the attention. Aside from Yellen, there are more than half a dozen Federal Open Market Committee (FOMC) members on the docket this week. Overseas, the May Ifo and ZEW data in Germany, along with retail sales and CPI data in Japan, will be the focus. The G7 Leaders Summit in Japan is Thursday and Friday, May 26 and 27.

Monitoring the Week Ahead

Monday

- Markit Mfg. PMI (May)

- Bullard (Hawk)

- Eurozone: Markit Mfg. PMI (May)

Tuesday

- New Home Sales (Apr)

- Germany (ZEW)

Wednesday

- Advance Report on Goods Trade Balance (Apr)

- Kashkari (Dove)

- Germany: Ifo (May)

Thursday

- Durable Goods Orders and Shipments (Apr)

- G7 Leaders Summit in Japan

- Japan: CPI (Apr)

Friday

- Consumer Sentiment and Inflation Expectations (May)

- Yellen (Dove)

- G7 Leaders Summit in Japan

Sunday

- Bullard (Hawk)

- Japan: Retail Sales (Apr)

Click Here for our detailed Weekly Economic Calendar

Important Disclosures

Past performance is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted.

The opinions voiced in this material are for general information only and are not intended to provide or be construed as providing specific investment advice or recommendations for any individual security. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

Stock investing involves risk including loss of principal.

Investing in foreign and emerging markets securities involves special additional risks. These risks include, but are not limited to, currency risk, political risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

Treasury inflation-protected securities (TIPS) help eliminate inflation risk to your portfolio, as the principal is adjusted semiannually for inflation based on the Consumer Price Index (CPI)—while providing a real rate of return guaranteed by the U.S. government. However, a few things you need to be aware of is that the CPI might not accurately match the general inflation rate; so the principal balance on TIPS may not keep pace with the actual rate of inflation. The real interest yields on TIPS may rise, especially if there is a sharp spike in interest rates. If so, the rate of return on TIPS could lag behind other types of inflation-protected securities, like floating rate notes and T-bills. TIPs do not pay the inflation-adjusted balance until maturity, and the accrued principal on TIPS could decline, if there is deflation.

Bank loans are loans issued by below investment-grade companies for short-term funding purposes with higher yield than short-term debt and involve risk.

Because of its narrow focus, sector investing will be subject to greater volatility than investing more broadly across many sectors and companies.

Commodity-linked investments may be more volatile and less liquid than the underlying instruments or measures, and their value may be affected by the performance of the overall commodities baskets as well as weather, disease, and regulatory developments.

Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

Investing in foreign and emerging markets debt securities involves special additional risks. These risks include, but are not limited to, currency risk, geopolitical and regulatory risk, and risk associated with varying settlement standards.

High-yield/junk bonds are not investment-grade securities, involve substantial risks, and generally should be part of the diversified portfolio of sophisticated investors.

Municipal bonds are subject to availability, price, and to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rate rise. Interest income may be subject to the alternative minimum tax. Federally tax-free but other state and local taxes may apply.

Investing in real estate/REITs involves special risks such as potential illiquidity and may not be suitable for all investors. There is no assurance that the investment objectives of this program will be attained.

Currency risk is a form of risk that arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

Technical Analysis is a methodology for evaluating securities based on statistics generated by market activity, such as past prices, volume and momentum, and is not intended to be used as the sole mechanism for trading decisions. Technical analysts do not attempt to measure a security’s intrinsic value, but instead use charts and other tools to identify patterns and trends. Technical analysis carries inherent risk, chief amongst which is that past performance is not indicative of future results. Technical Analysis should be used in conjunction with Fundamental Analysis within the decision making process and shall include but not be limited to the following considerations: investment thesis, suitability, expected time horizon, and operational factors, such as trading costs are examples.

This research material has been prepared by LPL Financial LLC.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial LLC is not an affiliate of and makes no representation with respect to such entity.

Not FDIC/NCUA Insured | Not Bank/Credit Union Guaranteed | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Securities and Advisory services offered through LPL Financial LLC, a Registered Investment Advisor

Member FINRA/SIPC

Tracking # 1-500005