Last week saw some huge drops from many large department stores thanks to disappointing earnings. Then on Friday, April retail sales came in at 1.3%, well above the consensus estimate. In fact, this was the best monthly gain since March 2015. So, which is it? Is the consumer dead or is there something else we are missing?

We asked LPL Research Chief Economic Strategist John Canally his take on all of this, and here is what he had to say:

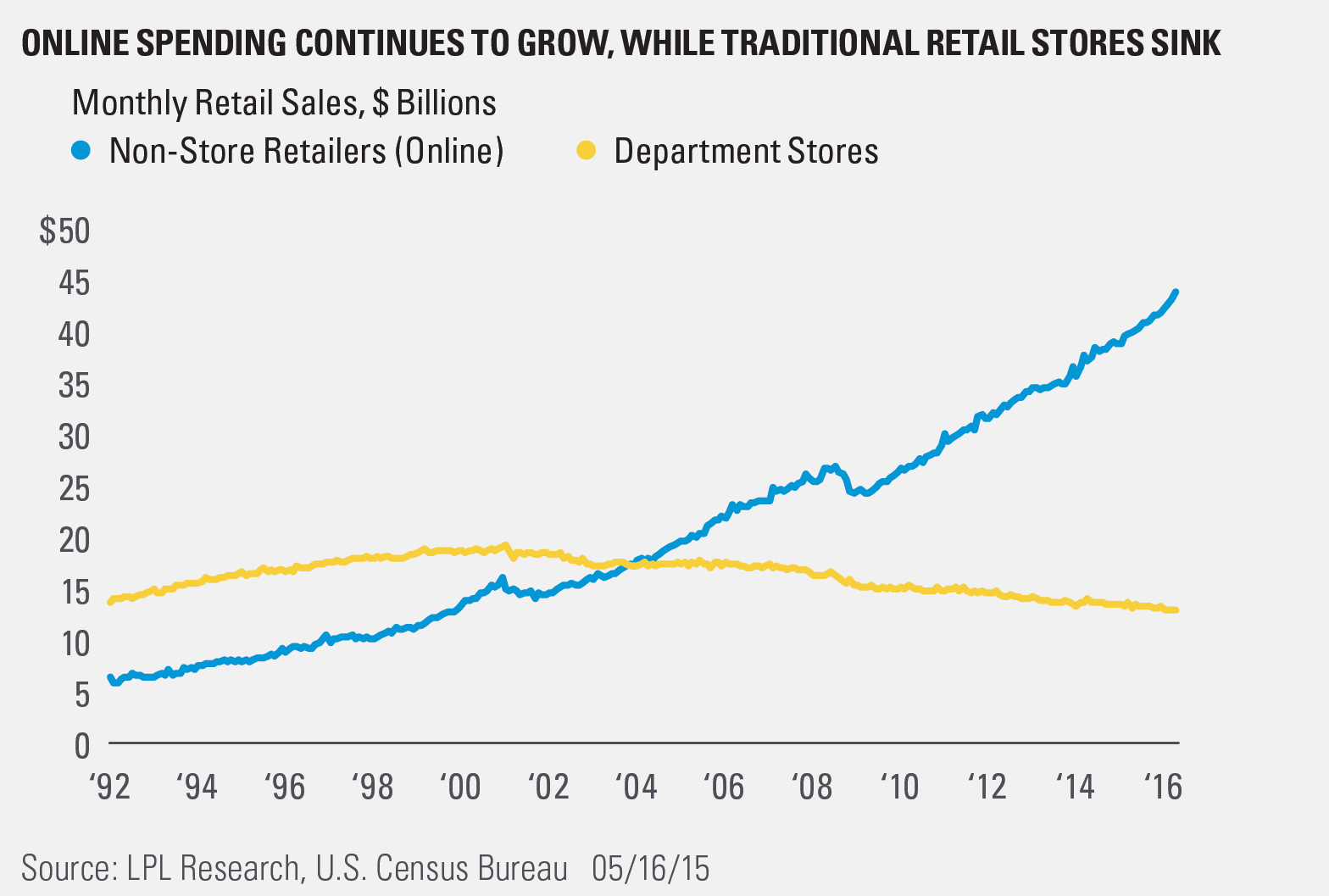

“Last week’s tepid news from mall-based retailers stood in sharp contrast to the 10% year-over-year gain in non-store retailers (online spending) reported in the U.S. government’s April retail sales report.”

In other words, online spending is soaring, while traditional department spending is stagnant. Here are a few stats to put all of this in better perspective.

- Total retail sales for department stores last month was $13.3B. Non-store retailers (online) had sales of $45.2B.

- Compared to department stores ($13.3B), gas stations saw sales of $32.6B last month, grocery stores had sales of $52.2B, and restaurants/bars came in at $54.1B. People are spending, just not at department stores.

- Incredibly, total monthly retail sales at department stores in January 1992 were $14.1B. Compared to the $13.3B for April, that’s a long time with no growth to show for it.

- Department stores and non-store retailers (online) sales were both $17.8B in November 2003. Since that time, non-store sales have surged +153%, while department stores have dropped 25%.

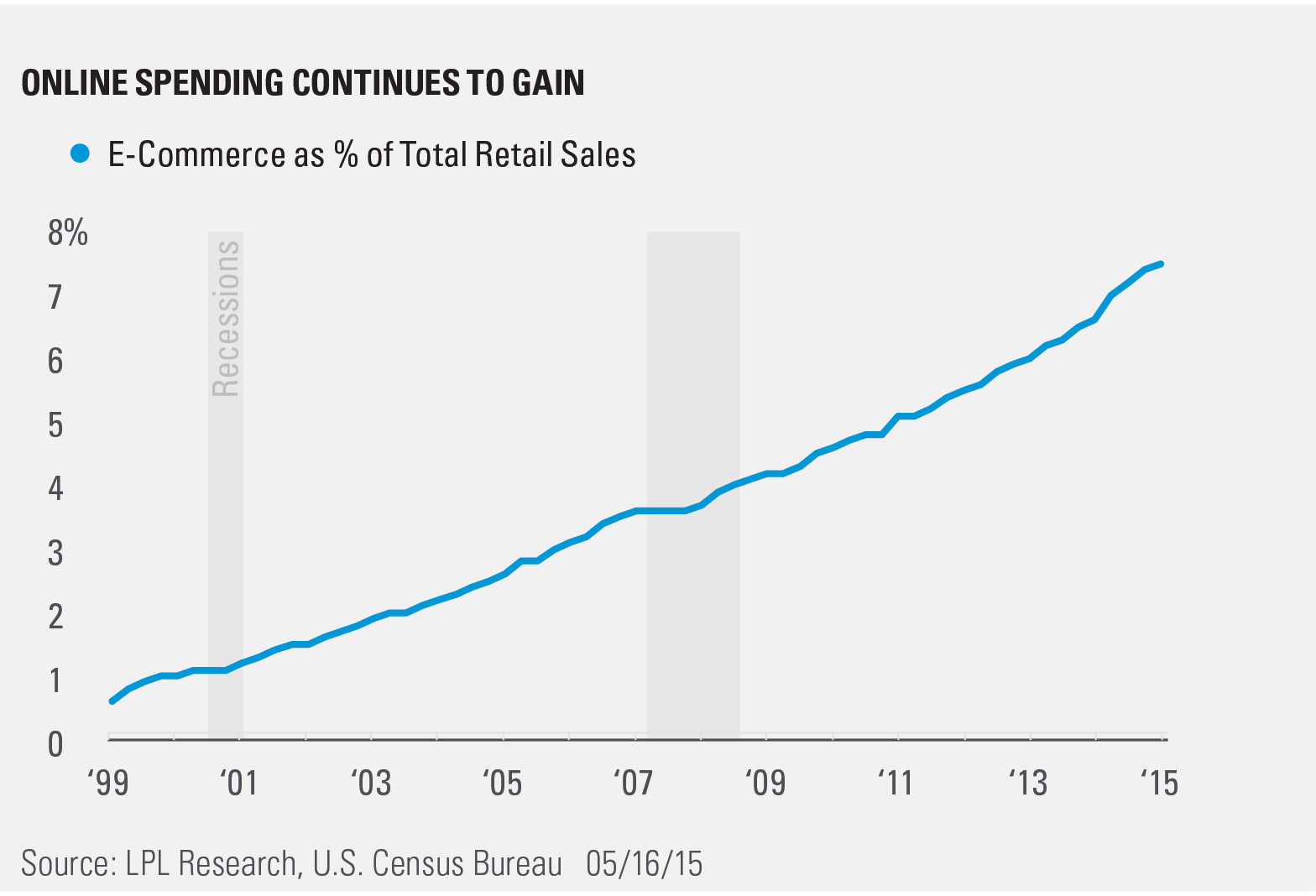

Lastly, according to recent data from the U.S. Census Bureau, e-commerce made up 7.5% of all retail sales during the fourth quarter last year. Incredibly, since this data started in late 1999, e-commerce as a percentage of retail sales hasn’t dropped for 64 straight quarters. It was 0.9% in the fourth quarter of 1999 and was up to 7.5% at the end of last year.

The U.S. consumer isn’t dead, spending habits have simply changed. For more on what we are seeing from the consumer now, be sure to read John Canally’s recent Weekly Economic Commentary, Consumer Check-In.

IMPORTANT DISCLOSURES

The economic forecasts set forth in the presentation may not develop as predicted.

The opinions voiced in this material are for general information only and are not intended to provide or be construed as providing specific investment advice or recommendations for any individual security.

This research material has been prepared by LPL Financial LLC.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial LLC is not an affiliate of and makes no representation with respect to such entity.

Not FDIC/NCUA Insured | Not Bank/Credit Union Guaranteed | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Securities and Advisory services offered through LPL Financial LLC, a Registered Investment Advisor

Member FINRA/SIPC

Tracking # 1-497997 (Exp. 05/17)